- CRE Daily

- Posts

- 2025 Apartment Supply: Top U.S. Markets to Watch

2025 Apartment Supply: Top U.S. Markets to Watch

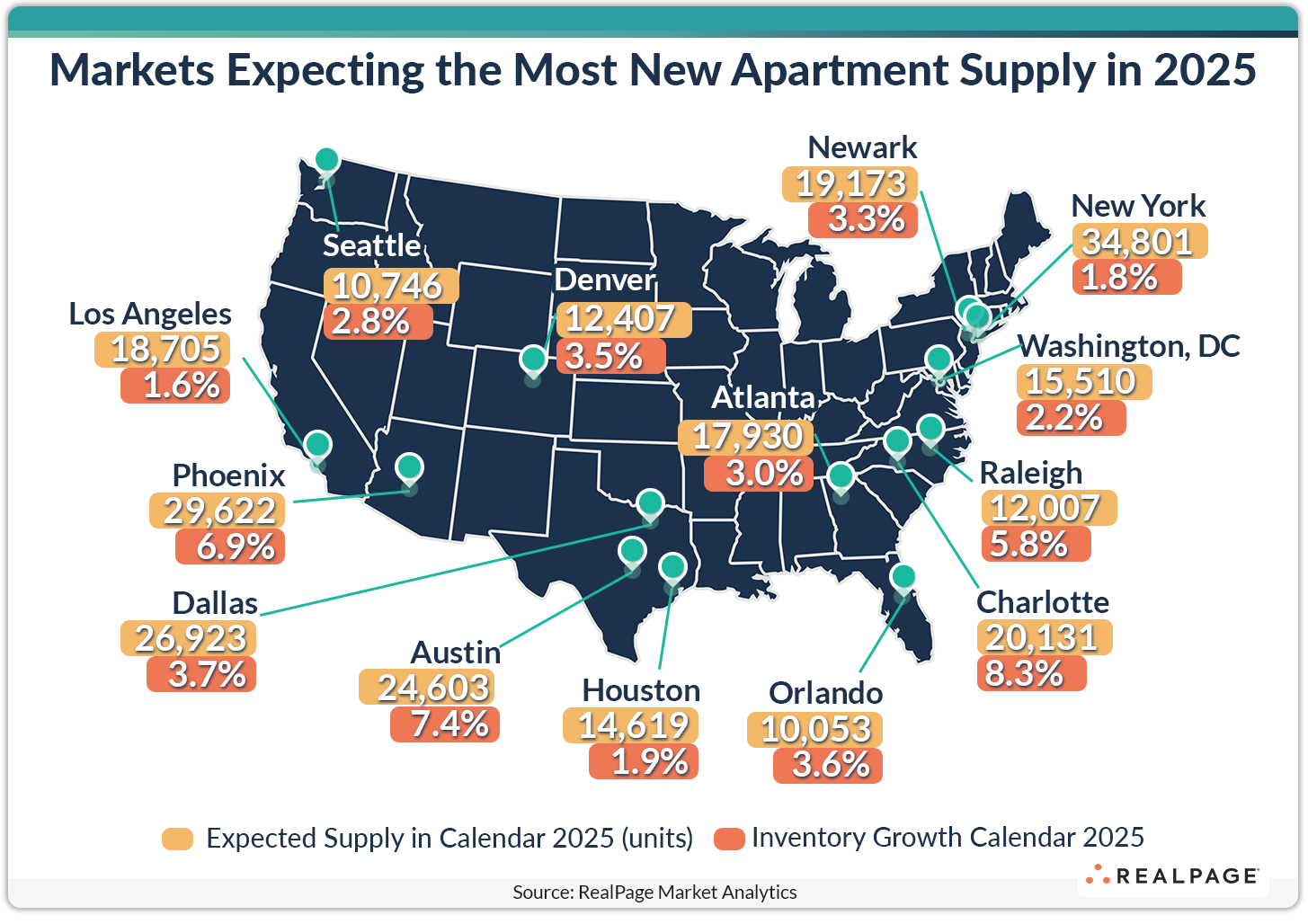

Over 500K apartment units are projected for 2025—the highest since 2008—with NYC leading deliveries at 35K units.

Jordan B.

November 26, 2024

Together with

Good morning. The U.S. apartment market is gearing up for a massive 2025, with over 500,000 new units set to reshape cities nationwide. Plus, scroll to the bottom to see the results from yesterday’s poll.

Today’s issue is brought to you by TractIQ—analyze every storage facility nationwide in just one click.

Market Snapshot

|

| ||||

|

|

Apartment Supply

NYC to Deliver Record 35K Apartments in 2025 of 500K Nationally

Over 500K apartment units are projected to be delivered in 2025, with The Big Apple leading in volume at nearly 35K units.

Bigger picture: According to RealPage, expect over 500K new apartment units next year nationwide—a record-breaking figure not seen since 2008. This is thanks in no small part to improving economic conditions (hint: upcoming Federal Reserve rate cuts), coupled with the fact that affordable homeownership remains out of reach for millions.

Zooming in: Around 14 US metros will each receive over 10K apartment units, with NYC leading the pack at a modest growth rate of 1.8%. Coming in second, Phoenix will see 29.6K units delivered at a 7% growth rate. And rounding out the top three, Los Angeles will add 19.4K units, its largest delivery load to date, at a 1.6% growth rate.

Sunny supply: The Sun Belt continues to drive national apartment supply growth. Texas metros, including Dallas, Austin, and Houston, will deliver 14–27K units each. Other leading markets in the region include Charlotte, Raleigh, Atlanta, and Orlando—all experiencing strong population and economic growth. Meanwhile, Seattle and Denver represent the West in high multifamily supply growth.

Small but strong: While major metros dominate in sheer volume, smaller markets are set to achieve the highest growth rates. Asheville, NC, will lead the nation with 13.3% more inventory, delivering over 3.5K units. Other small markets enjoying rapid growth include Huntsville, AL, Wilmington, NC, Savannah, GA, and Myrtle Beach, SC, which are expecting inventory growth rates above 7% next year.

➥ THE TAKEAWAY

Demand will dominate: The 2025 apartment market is set for recovery as supply pressures ease. Operators are betting big on Sun Belt growth, driven by strong job markets and high homeownership costs. With rents stabilizing, leasing conditions could rebound as early as spring, marking the end of a generational supply peak.

TOGETHER WITH TRACTIQ

Florida Tops the Nation in Self-Storage Development 📦🌴

Florida is setting the pace in self-storage construction, with 39MM NRSF in the pipeline—leading the nation. Texas (27MM NRSF) and California (25MM NRSF) round out the top three, as developers double down on self-storage, driven by strong returns despite rising interest rates.

The key? Knowing the competition.

With over 4,400 self-storage construction sites tracked across the U.S., TractIQ empowers investors, brokers, and operators with transparent data on new supply before it hits the market.

TractIQ also tracks demographics, rental rates, and other demand indicators such as residential construction sites, giving you a complete picture of the self-storage landscape to make smarter decisions.

Want to stay ahead? Access every storage facility nationwide, in just one click.

*Please see the advertising disclosure at the bottom of this newsletter.

✍️ Editor’s Picks

Major refi: Tishman Speyer is finalizing a $3B CMBS loan, led by J.P. Morgan, to refinance The Spiral, its 66-story Hudson Yards office tower, underscoring the resilience of Class A office assets.

Rate outlook: The MBA raised its 2025 mortgage rate forecast to 6.4–6.6%, citing inflation risks and tariff uncertainties, signaling challenges ahead for the housing market.

Very optimistic: US business activity hit a 31-month high in November, fueled by hopes for lower interest rates and pro-business policies under the incoming Trump administration.

Subdued deals: Net lease REIT acquisition volumes dropped 45% YoY in Q3, constrained by volatile capital costs and cautious equity signals, despite rising gross asset value premiums.

🏘️ MULTIFAMILY

More money moves: Floyd Mayweather Jr. invested $100M in a $3B joint venture with Go Partners, diversifying into luxury and affordable rental properties across iconic New York City locations.

Sun Belt strain: Multifamily developments in the Sun Belt face mounting challenges as overbuilding, stagnant rent growth, and rising vacancies strain finances.

Miami momentum: Clearline Real Estate secured $94.5M in financing for Excel Miami, a 24-story multifamily tower in the Art & Entertainment District, featuring 427 units and modern amenities.

Portfolio pivot: Pioneer Acquisitions is listing its 1,085-unit Hyde Park portfolio, spanning 21 properties near the University of Chicago.

Big Baltimore buy: Continental Realty acquired the 258-unit Dartmoor Place in Hanover, MD, for $86.5M, marking a high-profile multifamily sale in Baltimore’s competitive suburban market.

Community equity: Our Financial Health has launched a REIT targeting Harlem renters, allowing locals to take stakes in a 10-unit property with a $1K minimum investment.

🏭 Industrial

Industrial resilience: Despite high interest rates and declining deals, the Inland Empire market remains a national industrial leader with strong pipelines, strong rent growth, and rising PSF prices.

Sustainable growth: Galvanize Real Estate acquired a 608 KSF industrial property in East Windsor, NJ, leased to National Tree Co., with plans to enhance its value through decarbonization upgrades.

Mixed-use momentum: Gateway Classic Cars leased 43.8 KSF at Greystar’s Caliber industrial campus, part of a $500M mixed-use development in Peoria, AZ, set to include luxury housing and retail.

Strategic acquisition: LaSalle Investment Management acquired the 233.8 KSF Building I at Apex Commerce Center in Apex, NC, part of a growing four-building campus near Raleigh-Durham.

🏬 RETAIL

Exit strategy: Advance Auto Parts (AAP) is closing 70 SoCa stores and four West Coast warehouses as part of a full CA exit, citing inefficiencies in supply chain logistics.

Discount delights: Lightstone Group acquired The Outlet Collection Seattle for $82M and plans to invest $10M in upgrades, enhancing the nearly fully leased retail hub in Auburn, WA.

Retail expansion: ExchangeRight acquired a 13-property, 425 KSF retail portfolio from Tractor Supply in a sale-leaseback deal spanning nine states, further growing its net-leased asset portfolio.

🏢 OFFICE

Mega-project approved: Santa Clara greenlit Mission Point, a 48-acre mixed-use development by Genzon Group's US unit, featuring 3 MSF of office space and 1.8K homes (15% affordable).

Office maturity trends: October saw $1.75B in CMBS office loans mature with a payoff rate of 69%, highlighting improved outcomes for loans with debt yields above 8%.

Temporary debt relief: Office Properties Income Trust (OPI) secured refinancing for $340M in 2025 debt, pushing maturities to 2027 and avoiding bankruptcy, as it contends with mounting lease expirations.

🏨 HOSPITALITY

Hotel deals: The Cincinnati hotel market remains active with recent sales, including the 100-room Hampton by Hilton Inn & Suites in West Chester and Sonesta ES Suites.

A MESSAGE FROM CRE DAILY

CRE Daily Subscribers Get 10% Off + Free Shipping!

Searching for the perfect fit to this year’s holiday party or need some last-minute gifts for your team? We've got you covered. Shop our limited-edition ugly Christmas sweaters—CRE Daily's version.

Subscribers can enjoy 10% off with promo code CREDAILY and get free ground shipping on orders over $75!

*Please see the advertising disclosure at the bottom of this newsletter.

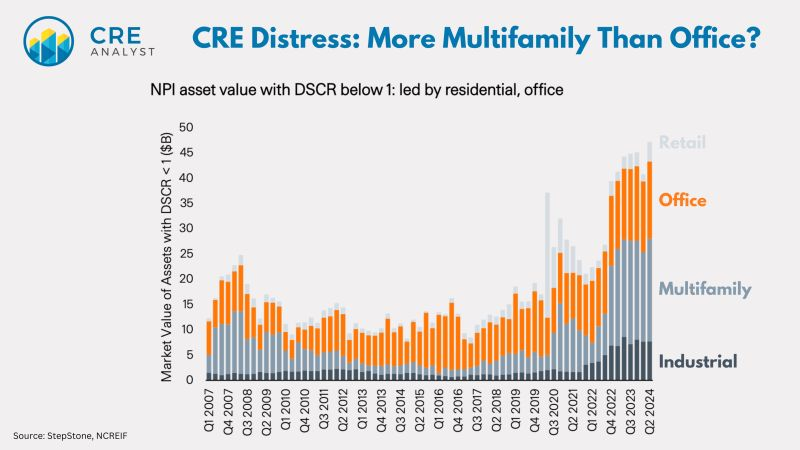

📈 CHART OF THE DAY

Another great chart from our friends over at CRE Analyst. Distress indicators show more pain ahead, with multifamily facing the biggest challenges. Defaults stem from LTV issues at maturity or DSCR stress over time, and NCREIF data reveals multifamily properties struggle most to cover debt service. StepStone warns declining rates won’t help this time—multifamily distress may be deeper than expected.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

Yesterday’s poll: What’s your take on NYC’s “City of Yes” plan?

🟩🟩🟩🟩🟩🟩 A much-needed step to tackle the housing crisis

🟨🟨🟨⬜️⬜️⬜️ Good, but too many compromises

🟨🟨🟨⬜️⬜️⬜️ Missed opportunity for bold reform

🟨⬜️⬜️⬜️⬜️⬜️ Not the right approach at all

Your two cents:

M.B: “Compromise is a part of negotiation and a win of this scale should be celebrated.”

D.S: “Regarding responsible development, governments need to have an "Attitude of YES".”

Y.G: “Your creating all these new units but have they even audited the current available units that are not being placed on the market? Some landlords make more money leaving a unit empty as opposed to rented in some of their rent stabilized units. Adding these many units is like a cold bath to communities.”

Reply