- CRE Daily

- Posts

- Alternative Lenders Fuel CRE Financing Rebound in Q1

Alternative Lenders Fuel CRE Financing Rebound in Q1

Non-bank lenders captured more than half of non-agency volume as capital markets regained momentum.

Nina Dale

May 13, 2026

In partnership with

Good morning. Commercial property lending came roaring back in Q1 as debt funds, improving leverage levels, and lower borrowing costs unlocked more deal activity. The result: the highest CRE lending momentum reading in five years.

🎙️This Week on No Cap: Equinox’s Jeff Weinhaus breaks down the real estate strategy behind the luxury fitness empire, from the 70/30 Rule that picks new cities to the long game with landlords that's let Equinox scale without losing its soul.

CRE Trivia 🧠

Most of the Las Vegas Strip isn’t actually in the City of Las Vegas. What unincorporated community contains most of the Strip?

(Answer at the bottom of the newsletter)

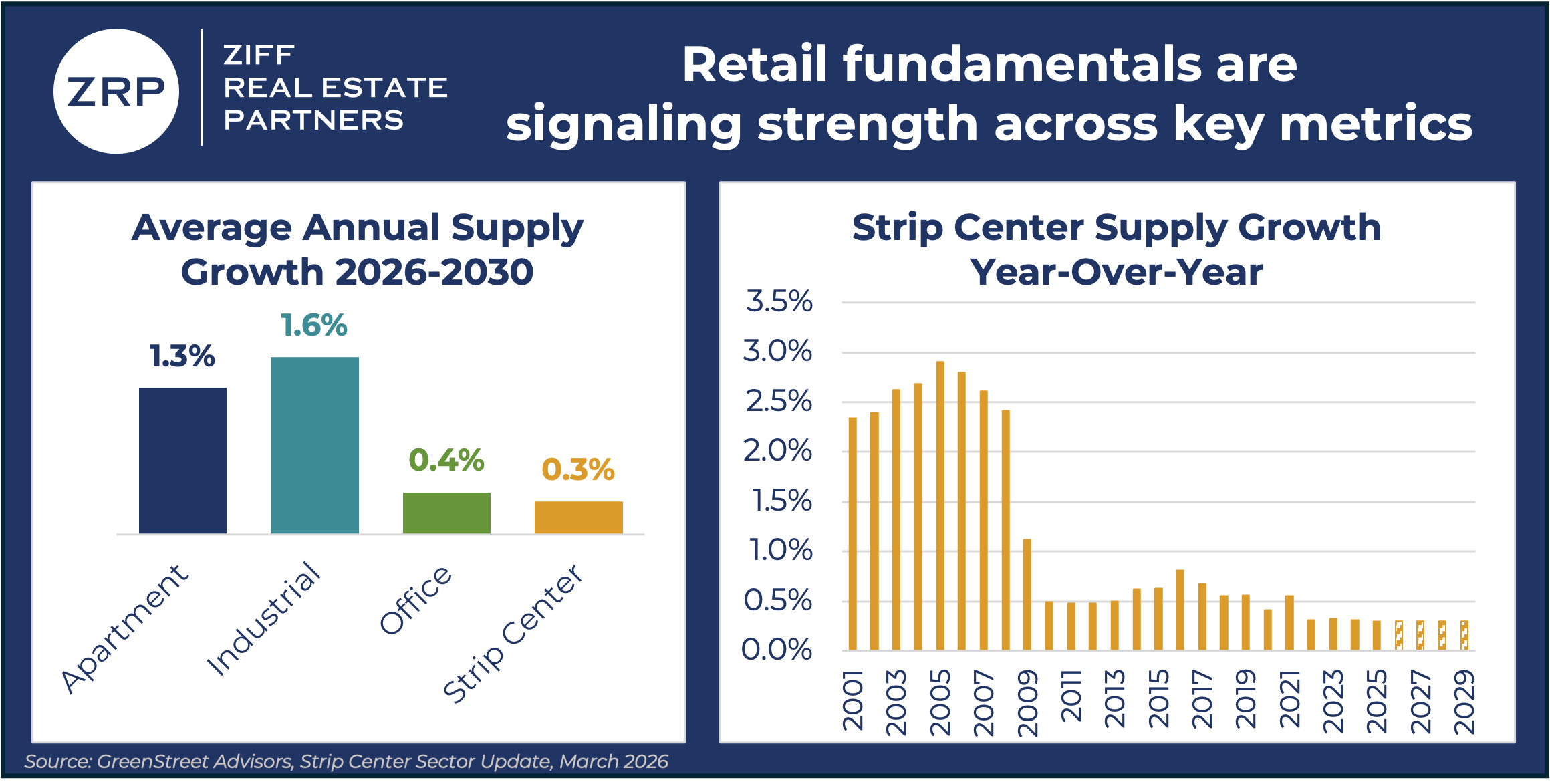

IN PARTNERSHIP WITH ZIFF REAL ESTATE PARTNERS

The Time for Retail is Now

For 35 years, Ziff Real Estate Partners has delivered strong returns across multiple market cycles. Today, the opportunity in necessity-based retail is as compelling as ever — undersupply and robust demand have made it one of the most attractive asset classes in commercial real estate.

ZRP is actively executing on this opportunity, having already closed $60M in retail acquisitions totaling 300,000 SF in 2026.

*This is a paid advertisement. Please see the full disclosure at the bottom of the newsletter.

Market Snapshot

|

| ||||

|

|

Lending Momentum

Alternative Lenders Fuel CRE Financing Rebound in Q1

Commercial real estate lending roared back in Q1 2026, with larger loan sizes, tighter spreads, and a wave of non-agency financing fueling the strongest momentum since 2021.

By the numbers: CBRE’s Lending Momentum Index climbed to 1.5 in Q1 2026, up from 1.2 in Q4 2025 and just 0.3 a year earlier, marking the highest reading in five years. Average loan sizes also jumped 14% year-over-year, signaling renewed confidence among borrowers and lenders alike.

Debt markets loosen up: Commercial mortgage spreads narrowed to 181 bps, while multifamily spreads tightened to 136 bps. Borrowing costs eased as average mortgage rates fell to 5.7%, and lenders grew slightly less conservative, with commercial LTVs rising to 61.5% and multifamily LTVs reaching 67.2%.

Alternative lenders dominate: Debt funds and mortgage REITs dominated non-agency lending in Q1, accounting for 53% of loan closings, up from 19% a year ago. Debt fund volume surged 280% YoY, while banks lost market share, falling to 22% from 34%.

Recaps drive activity: CBRE executives cited rising acquisition activity, improved price discovery, and fresh equity as key drivers of the rebound. Recapitalizations of large assets and portfolios remain active, with financing increasingly supporting joint ventures and alternative liquidity strategies beyond outright sales.

Multifamily financing remains strong: Government-backed lending remained a stabilizing force for apartment owners. Fannie Mae and Freddie Mac multifamily originations rose 35% YoY to nearly $30B in Q1 2026, while agency mortgage rates fell to 5.4%, improving borrowing conditions.

➥ THE TAKEAWAY

Expanding capital options: The CRE financing market is becoming more flexible and competitive, especially for well-structured deals. Borrowers now have more options beyond traditional bank financing and outright asset sales.

A MESSAGE FROM ARBOR REALTY TRUST

Top Markets for Multifamily Investment Report Spring 2026

Arbor Realty Trust's biannual report, developed in partnership with Chandan Economics, weighed 25 variables within 10 categories to pinpoint which of the nation's 75 largest metropolitan areas prove to be this spring’s most attractive locations for multifamily investment.

*This is a paid advertisement. Please see the full disclosure at the bottom of the newsletter.

✍️ Editor’s Picks

Automate every workflow from acquisitions to legal: AI-generated lease abstractions, investment memos, Excel models, and recurring reports. Trusted by JLL, Cushman & Wakefield, and AvalonBay. (sponsored)

Redemption reversal: Blackstone’s BREIT raised $1.2B in Q1 2026 while repurchase requests fell 41%, signaling a recovery as the fund expands into data centers and DST fundraising.

Ownership limbo: Young adult homeownership fell to 30% nationwide as rising housing costs push more than 9M Americans ages 25 to 34 to keep renting or live in someone else’s home.

Exchange engine: 1031 Crowdfunding is simplifying the race against IRS exchange deadlines with a fast-moving DST marketplace built for passive, tax-deferred real estate investing. (sponsored)

Capital squeeze: Rising data center costs are forcing smaller developers to sell assets, merge, or pull back while large investors with deeper capital continue expanding.

🏘️ MULTIFAMILY

Pipeline slowdown: U.S. apartment construction starts fell to 55K units in Q1 2026, down 73% from the 2022 peak, as high financing and development costs continue shrinking the pipeline.

Silicon surge: San Francisco apartment rents jumped 7.7% YoY — the strongest growth among major U.S. metros — as AI-driven tech hiring and limited new supply fuel demand.

HUD easing: HUD is cutting environmental review requirements for FHA multifamily loans to reduce delays and costs in housing development.

D.C. liquidation: Elme Communities lowered its payout estimate again as weak D.C. multifamily pricing pressures asset sale proceeds during its wind-down.

🏭 Industrial

Office shift: Panattoni acquired State Farm’s former 462K SF Tempe HQ for $37.5M to convert it into industrial space, adding to Phoenix’s rapidly growing wave of office-to-industrial redevelopments.

Chicago IOS: Realterm acquired a 28,985 SF industrial outdoor storage facility in Bridgeview, Illinois leased to Carrier, expanding its Midwest footprint.

Navy disposition: Prologis sold a 345K SF Tastykake HQ in Philadelphia’s Navy Yard to Bridge Investment Group for $87M, with the long-term bakery tenant remaining in place.

🏬 RETAIL

Retail pipeline: Simon Property Group detailed a $2B development pipeline as it leans on redevelopments amid record-low retail construction.

Newbury spree: Treeco bought $50M of Newbury Street and Massachusetts Avenue retail and office assets, expanding its Boston portfolio in a prime retail corridor.

Buc-ee’s expansion: Buc-ee’s is expanding into six new states with large-format travel centers as it continues its national rollout beyond Texas.

🏢 OFFICE

AI leasing: AI investment is accelerating CRE office demand across major tech gateways led by San Francisco and Silicon Valley with $578B in VC funding since 2020.

Tampa pivot: Tampa office absorption turned positive at 6K SF in Q1 2026 driven by renewals and flight to quality while rents rose to $28.72/SF and vacancy reached 16%.

Office pullback: Best Buy is raising in-office requirements to four days while marketing 313K SF of unused HQ space in Minnesota as it tries to boost collaboration and counter a 20% revenue decline.

Penn surge: Penn Station office district is drawing major tenants and rising rents, capturing 25% of NYC relocations.

🏨 HOSPITALITY

Hotel chill: Middle East conflict is clouding 2026 hotel outlook as RevPAR growth slows and higher fuel costs weigh on travel demand despite a strong Q1.

Shvo win: Shvo beat fraud and racketeering claims in a Core Club dispute at 711 Fifth Ave, with only a narrow $80K payment issue allowed to proceed.

Sheraton trade: A JV bought the 265-room Sheraton Suites Fort Lauderdale West in Plantation, planning a $10M renovation.

📈 CHART OF THE DAY

AI pricing adoption has surged since 2010, with AI pricing jobs rising from just 0.12% to 3% of all pricing roles by 2025, tracking the broader boom in AI hiring even as pricing jobs overall declined.

CRE Trivia (Answer)🧠

Paradise, Nevada. Created in 1950, the township kept casino tax revenue flowing to Clark County instead of the City of Las Vegas.

More from CRE Daily

📬 Newsletters: Stay ahead of the market with local insights from CRE Daily Texas and CRE Daily New York.

🎙️Podcast: No Cap by CRE Daily delivers an unfiltered look at the biggest trends—and the money game behind them.

🗓️ CRE Events Calendar: The largest searchable calendar of commercial real estate events—filter by city or sector.

📊 Market Reports: A centralized hub for brokerage research and market intelligence, all in one place.

📈 Fear & Greed Index: A fully interactive sentiment tracker on the pulse of CRE built in partnership with John Burns Research & Consulting.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |

Reply