- CRE Daily

- Posts

- Big Bank CRE Exposure Actually 40% Higher Due to REIT Debt

Big Bank CRE Exposure Actually 40% Higher Due to REIT Debt

US banks may have much higher CRE exposure than widely reported, due to overlooked REIT credit line lending.

Jordan B.

May 31, 2024

Together with

Good morning. US banks may have much higher CRE exposure than widely reported due to overlooked REIT credit line lending. Plus, the Fed’s Beige Book shows modest US economic growth since April.

Today’s issue is brought to you by Agora—your all-in-one real estate investment management platform.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

Market Snapshot

|

| ||||

|

|

Term loans & credit lines

Big Bank CRE Exposure Actually 40% Higher Due to REIT Debt

A recent study reveals that large US banks' CRE exposure is significantly higher when REIT debt is factored in, posing additional systemic risks.

Hidden exposure: Researchers, including Viral Acharya from NYU, have found that big banks' CRE lending risk grows by about 40% when accounting for term loans and credit lines provided to Real Estate Investment Trusts (REITs). This indirect exposure has largely been overlooked in risk assessments.

State of the market: REITs have struggled since the pandemic due to shifts like increased remote work, which affects office values, and rising borrowing costs impacting multifamily and office investments. This stress has led investors to pull money from trusts, causing liquidity issues for major players like Starwood Capital and Blackstone Inc.

Stress tests: REITs, needing to pay large dividends, often draw on bank credit lines during economic stress, creating sudden liquidity demands for banks. Researchers recommend that regulators include these exposures in stress tests to better gauge systemic risk. Currently, off-balance-sheet exposure has more than tripled since 2013, highlighting a significant regulatory gap.

Indirect lending: Banks can't easily manage the risks from REITs drawing down credit lines at will, which can amplify cyclical risks. This "collateral damage" suggests that systemic risk from CRE exposure is greater than previously thought. The study notes that office distress was over $38B by the end of 2023, with another $50.3B listed as potentially distressed, according to MSCI.

Zoom in: Morgan Stanley, among the largest US banks, has the highest percentage of its credit lines committed to REITs, though its exposure is smaller in absolute terms compared to peers. The Fed noted a 5% year-over-year decline in bank credit commitments to REITs in its April financial stability report, yet the growth rate of these credit lines has outpaced other borrowing sectors.

➥ THE TAKEAWAY

Big picture: The study suggests banks should charge higher fees for credit lines to REITs to offset the increased risk. Blackstone REIT's experience highlights this, as they secured increased credit lines with minimal spread changes despite elevated risks. As of Q4 2022, large US banks had $345 billion in indirect CRE exposure, up from $109 billion in 2013. Despite this, REITs maintain relatively low leverage ratios, which might shield them somewhat from financial stress.

TOGETHER WITH AGORA

Read Agora's product review on CRE Daily

Looking to transform your real estate investment management processes?

Agora’s comprehensive platform is designed to streamline your operations and elevate your operational efficiency.

From a customizable Investor Portal and CRM to financial automation, Agora empowers companies to raise and preserve capital while providing their investors with the best real estate investment experience.

Discover how Agora can help you manage investors, simplify fundraising, and ensure seamless operations.

✍️ Editor’s Picks

Modest price push: The Fed’s Beige Book shows modest US economic growth since April. Consumers are resisting higher prices, with slight job gains reported.

Hurricane season 2024: Nearly 33M properties are at risk from Texas to Maine as hurricane season approaches. Damages could cost $10.8T, with an active season predicted.

Construction caution: Citigroup downgrades Bank OZK (OZK) due to concerns over its $1B+ in loans, leading to a 14% share price drop.

Industrial lending boom: CRE debt originations stabilize with a mere 2% YoY decline in Q1, as industrial leads lending with 49% more loans.

🏘️ MULTIFAMILY

Luxury renovations: A private investor bought Lennox at West Village in Uptown Dallas for $39M to renovate and attract upscale tenants.

Investing in value: Lion Real Estate Group acquired a 225-unit class B apartment complex in Charlotte for an undisclosed price and is planning for upgrades.

How much lower? Only $5B in multifamily sales were reported by the end of Q1, the lowest quarterly figure since 2Q20’s $4B, and 61% lower YoY. Are we near the bottom yet?

Small but mighty: Demand for smaller multifamily properties is rising, particularly for units with up to 12 units.

🏭 Industrial

Building completed: Terreno Realty Corp. completed Phase IV Building 40, a 186KSF facility in Hialeah, FL, investing $43.8M with a 6.3% cap rate.

More where that came from: Blackstone's (BX) Link Logistics is planning a 1.1MSF complex near Tesla's Austin gigafactory, adding to the booming industrial growth in the area.

Deal of the day: Somerset Properties and Waterfall Asset Management sold a Charlotte distribution center for $97M, setting a state record.

🏬 RETAIL

Discount duel: Dollar Tree (DLTR) bids for 93 99 Cents Only California locations out of 112 total stores, pending the discount retailer’s bankruptcy court approval.

Waiting for good deals: A private equity firm bought the Horizon Village shopping center in Phoenix for $15.6M at $137.75 PSF.

M&A of the day: T-Mobile (TMUS) just announced that it will acquire most of U.S. Cellular’s (USM) wireless operations and assets for $4.4B.

🏢 OFFICE

Sky-high lease: Fintech Pontera Solutions Inc. just signed a 40.7KSF lease at the Empire State Building in Midtown Manhattan.

Stock exchange save: Property & Building Corporation used the Tel Aviv Stock Exchange to pay off a $385M loan from JPMorgan Chase (JPM).

Looming AI threat: Q1 witnessed the lowest office building occupancy rates on record, with over 1BSF at risk of obsolescence. On top of that, AI could replace up to 85M jobs by 2025.

Seattle weather: Martin Selig Real Estate faces default on $239M in loans for 7 Seattle office buildings, now at 69% average occupancy.

🏨 HOSPITALITY

Rooftop revelry: Miami's Juvia Group signed a 15-year rooftop restaurant lease at Standard Residences in Midtown Miami for a new concept restaurant called Solana.

Oil money: A Chicago-based oil businessman and NexGen Hotels bought the 137-key Hotel Versey at 644 West Diversey Parkway in Chicago.

A MESSAGE FROM OPAL HOTELS GROUP

Opal Hotels Group, a private real estate investment company with 9 hotels in the Eastern U.S., is excited to offer a unique co-investment opportunity in a 95-room TownePlace Suites by Marriott.

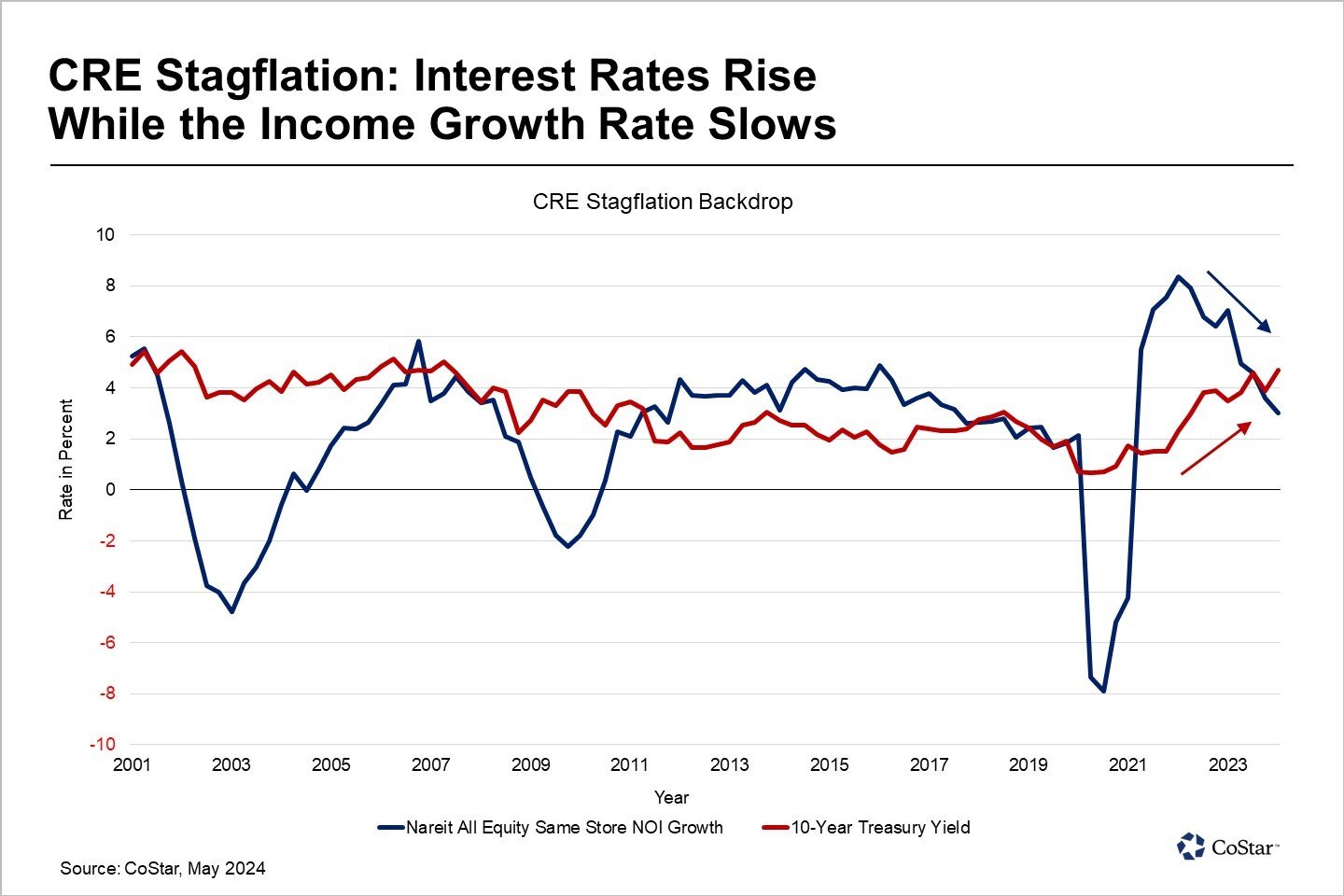

📈 CHART OF THE DAY

According to CoStar, stagflation may well be on the horizon, thanks to a dipping Nareit All Equity Same Store NOI Growth index and a rising 10-Year Treasury Yield.

In fact, the two trendlines just performed a ‘death cross’ that may mark higher interest rates for longer and slowing income growth.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |

Reply