- CRE Daily

- Posts

- California Banks Are Most Exposed to Commercial Property

California Banks Are Most Exposed to Commercial Property

127 banks registered in the state have property debts exceeding 300% of their value, the highest number in the US.

Jordan B.

April 12, 2024

Together with

Good morning. California regional banks face risks due to high CRE exposure and rising foreclosure rates. Meanwhile, multifamily securitizations are under the spotlight. We break down the top 25 MSAs.

Today’s issue is brought to you by QC Capital. Become an investor in the booming car wash industry.

Market Snapshot

|

| ||||

|

|

BAD DEBT

California Banking Sector Faces More CRE Challenges

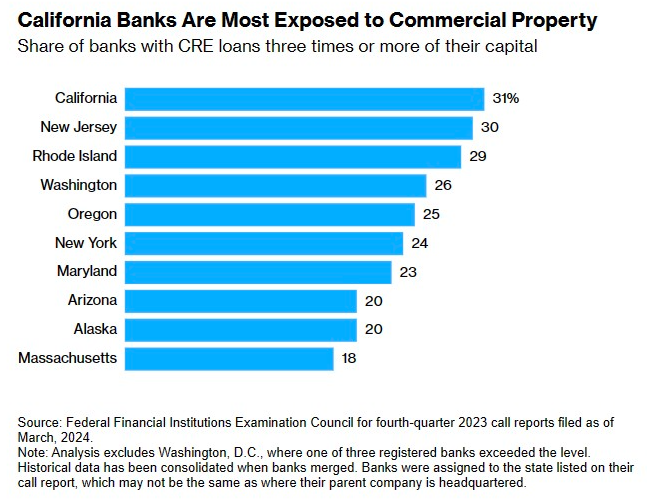

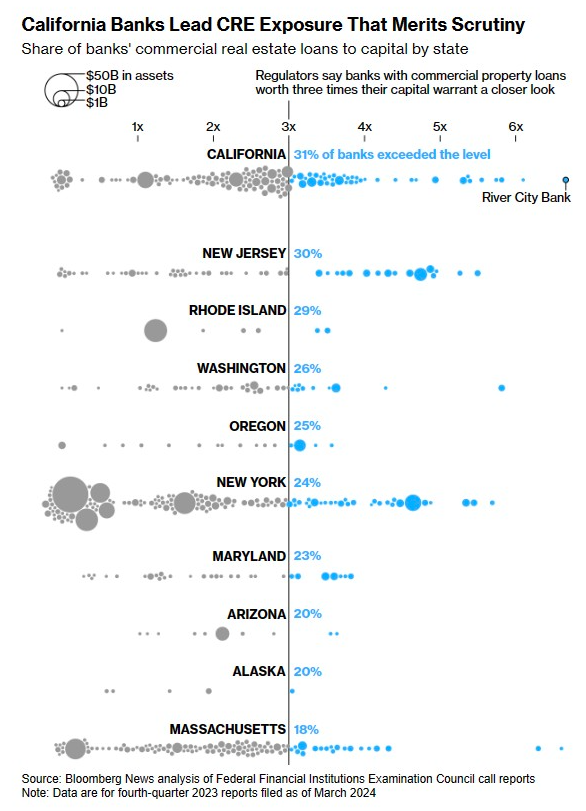

One year after the collapse of SVB, California banks are once again in the spotlight due to their outsized exposure to CRE investments, raising concerns about potential risks and losses.

What happened: California banks are showing the highest concentration of commercial real estate loans relative to their capital in the U.S. Nearly a third of the state's banks have property debt that exceeds 300% of their capital, a benchmark often flagged for increased regulatory attention. The backdrop is a commercial property market under pressure from the highest interest rates in decades, leading to a heightened risk for banks as loan defaults increase.

Over the limit: California could rank as the world's fifth-largest economy, yet its banking sector is fragmented. Wells Fargo is the only major bank headquartered in the state. Regional banks, heavily reliant on commercial real estate, lack diversified revenue streams, which increases risk. High concentrations in specific client types, like venture capital or wealthy individuals, have led to significant failures, exemplified by Silicon Valley Bank and First Republic Bank.

In the spotlight: River City Bank in Sacramento has been particularly aggressive, growing its assets to approximately $5 billion over five years. Despite the bank's claims of cautious lending, its CRE loans now stand at 660% of its capital, the highest among all banks in California—but the lender is not alone. Almost 30% of the CA’s 127 registered banks have property debt exceeding 300% of capital.

➥ THE TAKEAWAY

Big picture: California's regional banks are under stress as a softening property market and rising interest rates lead to increased vacancies and falling property values. These challenges have forced banks to strengthen their balance sheets against potential bad loans. With the CRE market facing growing pressures, regulatory bodies like the Federal Reserve and the Office of the Comptroller of the Currency are intensively monitoring to prevent another collapse.

TOGETHER WITH QC Capital

Earn ~12% Annual Cash Flow With Our Car Wash Fund 1

Unlock the potential for consistent returns and sustainable growth in the thriving car wash industry with QC Capital Car Wash Fund I. Here's why accredited investors are diving in:

🟠 Investment Appreciation Advantage: Car wash investments offer significant potential for appreciation driven by location, demand, and efficiency.

🟠 Depreciation Deductions: Enjoy substantial tax advantages and increased cash flow through depreciation deductions.

🟠 1031 Exchange Eligibility: Qualify for tax-deferred reinvestment and portfolio growth with 1031 exchanges.

🟠 Asset Appreciation: Benefit from long-term wealth accumulation through infrastructure upgrades and market trends.

🟠 Passive Income Potential: Diversify your portfolio and achieve financial goals with steady cash flow from memberships and service fees.

*Please see the advertising disclosure at the bottom of the newsletter.

✍️ Editor’s Picks

Rising homeownership costs: Homeownership costs in the U.S. have surged, with insurance costs up 63% as rising property taxes and maintenance fees impact affordability.

CEO bets on leases: Vornado's (VNO) CEO Steve Roth avoids gambling on downstate casino licenses due to higher financial priorities and low odds for Manhattan.

Insurance hurdles: Insurance challenges are causing real estate investors to abandon deals, impacting opportunities, per the Spring 2024 Investor Sentiment Survey.

Changing of the guard: Chris Ludeman, CBRE's global capital markets president and a four-decade CRE veteran, will step down on May 1 but remain as a senior adviser through year-end.

🏘️ MULTIFAMILY

Bold move: Blackstone's (BX) takeover of Apartment Income REIT (AIRC) spurs the biggest apartment rally since December, with AIRC surging 22%.

Rental rush: Many Americans struggle with rising home costs and low inventory due to hedge funds buying affordable homes.

Apartment auction: After holding on since 2019, Food First is throwing in the towel and ready to sell 20+ rent-stabilized buildings via Maltz Auctions.

Out with the old: A 104-year-old row home in Philly's Francisville collapsed due to adjacent construction, resulting in an emergency demolition.

Housing equality: LA considers a new "fair chance" ordinance that would prohibit landlords from using criminal history to qualify renters and face fines for discrimination.

Dynamic duo: Aflalo Equities, partnering with Harkham Family Enterprises, plans to develop four Beverly Hills properties for residential and retail use.

🏭 Industrial

Filling in the gaps: NorthBridge Partners and Park Madison Partners closed NB Partners Fund IV with $950M, focusing on infill logistics properties.

Office space race: Investors are converting SoCal office buildings to industrial due to a tightening market. As an example, Orange County’s industrial vacancy stands at 2.8%.

Industrial fortunes: Powerline Commerce Park in Deerfield Beach, FL, sold for $18.1M at $248 PSF, featuring 72.9KSF.

🏬 RETAIL

Tech brews: Starbucks (SBUX) plans to redesign stores, focus on global expansion, and save $3B, aiming for 55K locations by 2030.

Retail roulette: Macy's (M) may end up agreeing to a $6.6B buyout offer, with activist investors valuing its nationwide property footprint at $5B to $14B. But is it really worth it?

🏢 OFFICE

Crumbling capital: St. Louis' 44-story AT&T Tower, originally sold for $205M, resold for just $3.6M, plummeting in value by over 98%.

Office slump: Office visits in March were down 32.7% compared to March 2019, although landlords are seeing lease renewals increasing.

Rent rocket: South Florida office rents rise, with Miami up 9.1% to $60.28 PSF YoY. However, leasing activity is mixed, with Palm Beach, Broward declining.

Tightening grip: Fortress Investment Group buys a $22.2M loan for a 40.1KSF office building, potentially gaining property control.

🏨 Hospitality

Hotel handover: Fisherman’s Wharf Hotel in San Francisco goes back to its lender after DiNapoli Capital Partners defaulted on an $85M mortgage.

Refinance: Blackstone has secured a $428.5 million floating-rate refinance from Morgan Stanley and Société Générale for a 23-hotel portfolio. The loan includes potential extensions and is set for securitization in the BX 2024-BRVE CMBS deal.

Restaurant renaissance: Sun Belt cities are enjoying more seated diners than before the pandemic, with Houston (+9.3%), Phoenix (+12.6%), Austin (+23.1%) and Miami (+50.4%) in the lead.

Rental ruckus: A legal battle erupts as Stockdale Capital Partners sues MJW Investments over an allegedly inflated $62.2M appraisal for Le Merigot.

Family affair: Developer David Martin acquires a 25% interest in Miami Beach's former Deauville Beach Resort site for $12.5 million, hinting at future iconic development plans.

PROPERTY REPORT

Evaluating Multifamily Market Risks Across Major MSAs

Multifamily securitizations are under the spotlight. A recent analysis by KBRA, utilizing Trepp data, has provided a detailed risk assessment of multifamily markets in 25 major metropolitan statistical areas (MSAs).

Digging into the data: The analysis hinges on $189.1 billion worth of multifamily assets, representing about two-thirds of the $287.8 billion tracked in various Freddie Mac K-Series and other CRE financial products. Cities were rated on a 100-point scale, where a higher score indicates greater risk to investors.

By the numbers: The riskiest markets include Detroit, MI (86); Chicago, IL (79); Denver, CO (77); Washington, D.C. (74); Atlanta, GA (74); and Philadelphia, PA. In contrast, the most stable markets are Las Vegas, NV (30); San Diego, CA (48); Houston, TX (48); San Francisco, CA (52); Portland, OR (52); and Riverside, CA (52).

Risk criteria: KBRA's risk assessment considered factors such as loan balances, loan maturity profiles, vacancy rates, ongoing construction activities, and economic forecasts, including employment and population growth.

➥ THE TAKEAWAY

Why it matters: Insights reveal that cities like Detroit and Chicago are impacted by low employment and negative population growth trends, while Denver's challenges stem from above-average vacancy rates and construction activities. Meanwhile, cities like Austin, Phoenix, and Charlotte were spotlighted for their high vacancy and construction rates, yet they showed resilience thanks to strong market demand indicators.

📈 CHART OF THE DAY

The recent surge in leasing activity in Central Florida has led to significant absorption gains and rapid rent increases. However, this strong demand has resulted in a shortage of available spaces, particularly in the size range most preferred by industrial users.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |

*Advertising Disclosure: Under no circumstances should any material at this site be used or considered as an offer to sell or a solicitation of any offer to buy an interest in any investment. Past performance may not be indicative of future results. An investment in commercial real estate is speculative and subject to risk, and there can be no assurance that the future performance of any specific investment, investment strategy or selection of a specific property as referenced in the information herein, will be profitable, equal any corresponding indicated historical performance level(s) or be suitable for your needs. Due to various factors, including changing market conditions, this content may not be reflective of current opinions or positions. We encourage our readers to conduct their own research and consult with professional advisors before making investment decisions.

Reply