- CRE Daily

- Posts

- Commercial Properties Face $2.2 Trillion Debt Deadline

Commercial Properties Face $2.2 Trillion Debt Deadline

More than $2.2 trillion in debt is maturing before 2028. Expect a flurry of debt restructurings and strategic negotiations.

Jordan B.

January 18, 2024

Together with

Good morning. A record amount of CRE debt is maturing, leading to potential defaults and higher refinancing rates. Meanwhile, the retail market in Dallas reached an all-time high occupancy rate of 95.2%.

Today’s issue is brought to you by Bullpen. Hire the top 3% of real estate talent.

📊 Fear and Greed Survey: Your insights are needed. Please take 3 minutes to provide your perspective on the current mood within the CRE industry and your predictions on future price trends.

Market Snapshot

|

| ||||

|

|

Turbulent Times

Rising Rates, Mounting Debts - The $2.2 Trillion Dilemma Facing Commercial Real Estate

The commercial real estate market is at a crossroads, with a record $2.2 trillion in debt maturing by 2028, which could lead to a surge in defaults as borrowers are forced to refinance at higher rates.

What happened: In 2023, an unprecedented $541 billion in commercial real estate debt came due, a record for a single year. Many property owners managed to extend their loans, capitalizing on one- or two-year options included in their original agreements. However, these extensions are nearing their end, forcing borrowers to face a new landscape of higher rates and declining property values.

Pandemic's lingering impact: The sector is still grappling with the repercussions of early pandemic agreements, where payments were deferred. Unlike home mortgages, CRE mortgages are mostly interest-only, meaning borrowers have to refinance or pay off the principal when debt matures. With rates on the rise, borrowers must refinance at much higher rates than their maturing loans. Meanwhile, even multifamily is suffering from higher vacancy, making it hard to raise rents or make payments on floating-rate debt.

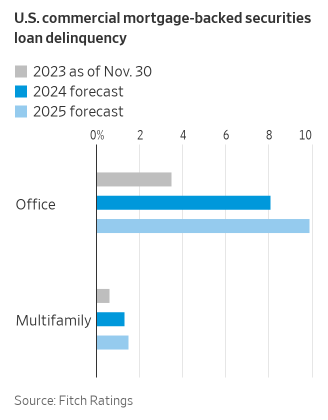

Rising delinquency: Fitch Ratings anticipates a sharp increase in delinquencies, projecting a jump to 4.5% in 2024 and 4.9% in 2025, significantly higher than the 2.25% rate seen in November 2023. This trend is causing alarm among financial regulators, who fear a potential ripple effect on the broader financial system and a reduction in property tax revenues.

The refinancing challenge: Refinancing remains the preferred option for maturing loans, but disagreements between lenders and borrowers over property values are complicating these discussions. More than $50 billion of the maturing loans this year are from nonbank lenders, adding to the complexity.

Workout negotiations: Those who fail to extend their loans may have no choice but to play a losing hand. The weak property sales market makes negotiations challenging. Lenders, considering worst-case scenarios, are less inclined to take risks. The result: more workout negotiations, where borrowers may have to contribute additional capital or, in some cases, hand over the keys to creditors.

➥ THE TAKEAWAY

What comes next? Rising interest rates and maturing CRE debt have created a challenging and unforgiving environment for borrowers and lenders alike. Refinancing at higher rates, combined with vacancies and weakening cash flows, has put significant pressure on property owners. Additionally, delinquency rates are expected to rise, increasing the risk of defaults. Workout negotiations may be the only solution.

SPONSORED BY BULLPEN

Whether you’re on your third investment or your 30th, the right team is the difference between lightning growth and stagnation.

Unfortunately, hiring experts takes time away from things like finding deals, raising funds, and executing projects.

That’s where Bullpen comes in. As a team of commercial real estate veterans, we know how important it is to find the right talent at the right time.

Freelance, fractional, or full-time commercial real estate experts - we can help staff your team for any stage of growth.

Are you ready to take your team to the next level? Hire now.

✍️ Editor’s Picks

Red-hot market: Despite a volcanic eruption destroying hundreds of homes, Puna District in Hawaii is now the fastest-growing region on the islands due to affordable land prices.

REIT retreat: Brookfield Real Estate Trust, which primarily focuses on rentals and logistics, suffered a 6.7% annual loss, due to valuation adjustments and interest rate impacts.

Bidding buzz: Improved market trends seen in late 2023 have sparked increased bidding activity and a narrowed bid-ask spread this year.

Defaulted dreams: Blackstone's (BX) defaulted $308M loan for a Midtown Manhattan office is being sold at a 50% discount, potentially for an office-to-residential conversion.

Poached: Avi Kollenscher, a former Nightingale executive, joins Capstone Equities as partner and COO amid Nightingale's legal and financial troubles.

🏘️ MULTIFAMILY

Radisson renovation: Oakland Alameda Hotels plans to convert a 300-room Radisson near Oakland Airport into affordable homes, with kitchenettes in each unit.

Mansion tax exodus: LA's mansion tax prompts wealthy Angelenos to search for lower taxes in out-of-state markets. Nobody should be surprised.

Conversion accelerator: 46 buildings in NYC's Office Conversion Accelerator program are expected to create 2,100 housing units this year.

Building back up: Multimillion-dollar developments are defying high rates, with projects like a 1,647-bed student housing in Knoxville and a 399-unit residential tower in NYC.

From manufacturing to multifamily: A new plan for rezoning 5 blocks along Park Avenue in Bedford-Stuyvesant proposes 560 apartments and 3 yeshivas.

🏪 RETAIL

Innovating beauty: Ulta Beauty's (ULTA) CEO discusses the retailer's innovations and the expected growth of the beauty market this year.

Breaking barriers: Charlotte-based Aston Properties acquires high-profile shopping center McBee Station in downtown Greenville, becoming one of the largest retail owners in the area.

🏢 OFFICE

Renewed leases: NACo and NLC sign lease renewals for 78KSF of office space at 660 North Capitol NW in Washington, D.C., acquired by Eagle Cliff for $30M.

Shrinking tenants: Office occupiers anticipate a 3% drop in their SF footprints this year, according to a survey by Corenet Global and Cushman & Wakefield.

Mismatched expectations: A recent report shows that converting office buildings into multifamily properties is rare and usually not very successful.

Trophy office demand: High demand for top-quality offices in major markets like Miami, DC, NYC, and Chicago is not being met by new supply, as lenders are reluctant to finance new projects.

RETAIL RECORD

DFW Retail Market Hits All-Time High Occupancy in 2023, Greater Potential in 2024

According to Weitzman's 2023 Shopping Center Survey, the Dallas-Fort Worth retail market achieved its highest occupancy rates in history.

The findings: 2023 saw the DFW retail real estate reach an all-time high occupancy rate of 95.2%. Dallas alone, battling the e-commerce wave, achieved a 95% occupancy rate, a significant jump from 93.8% in 2022. The city boasts 137 MSF across 1,001 projects. Fort Worth isn't far behind, with a 95.5% occupancy rate across 62.3 MSF. Austin, Houston, and San Antonio also posted impressive numbers, but DFW's growth is the talk of the town.

Leading the way: Grocery stores are the linchpins of DFW's retail market, particularly Kroger, Tom Thumb, and H-E-B, driving DFW's retail leasing, with 488 properties totaling 74.1 MSF. Retail giants like Sprouts, Barnes & Noble, Nordstrom Rack, and fitness brands filled large vacancies, contributing to 1.8 million square feet of net leasing in 2023. New developments added over 1 million square feet, surpassing 2022's 539,000 square feet, with high rents indicating a robust market despite elevated construction costs.

➥ THE TAKEAWAY

Growing stronger: Weitzman's 2024 forecast for North Texas is optimistic: occupancy levels are expected to reach around 95.8%, with net absorption at 2.2 million square feet and approximately 2 million square feet of new developments. The demand for well-located vacancies and the active expansion of anchor stores—and grocers, in particular—should contribute to the push for new construction and infill redevelopment in the region for years to come.

CHART OF THE DAY

In 2023, a significant portion of new apartments in the U.S. emerged in the South, a trend continuing into 2024 with about 53% of completions in this region. Texas is a major player, with Dallas, Austin, Houston, and Charlotte each expecting over 20,000 new units.

The West follows, contributing 27% of national supply, led by Phoenix, Denver, Los Angeles, and Seattle. The Northeast and Midwest will see less growth, with New York and Newark in the Northeast doubling their 2023 delivery pace in 2024. However, the Midwest lacks any market in the top 10 for 2024 deliveries, with Minneapolis and Chicago leading the region's moderate growth.

Source: RealPage

What did you think of today's newsletter? |

Reply