- CRE Daily

- Posts

- Freddie and Fannie Face Rising Delinquencies and Fraud Risks in Q3

Freddie and Fannie Face Rising Delinquencies and Fraud Risks in Q3

Fannie Mae and Freddie Mac both reported rising delinquencies in Q3 2024, driven by economic pressures and an unfolding mortgage fraud investigation.

Jordan B.

November 05, 2024

Together with

Good morning and happy Election Day. Freddie Mac and Fannie Mae’s Q3 results show steady growth in multifamily financing—but also rising delinquencies and a wave of new fraud risks that could impact future lending practices.

Today's issue is sponsored by Reap Capital.

🎙️ Tune in to the No Cap season finale! Hosts Jack Stone and Alex Gornik chat with Richard Byrne, President of Benefit Street Partners, to dive deep into his career and discuss his insights on direct lending, distressed opportunities, and real estate debt markets.

Market Snapshot

|

| ||||

|

|

DELINQUENCIES RISING

Freddie Mac and Fannie Mae Report Rising Delinquencies, Heightened Fraud

Freddie Mac and Fannie Mae saw rising multifamily delinquencies in Q3, as Fannie also flagged major mortgage fraud risks as an ongoing headwind in lending.

By the numbers: Fannie Mae’s delinquency rate rose from 0.48% in Q2 to 0.52% by September, marking a steady climb throughout the year. Freddie Mac’s rate, while more stable, increased slightly to 0.39% by quarter-end, with delinquencies largely affecting floating-rate loans and small-balance properties.

Fraud risks: For the first time, Fannie Mae disclosed financial losses related to mortgage fraud as it intensified its investigation into fraudulent multifamily lending transactions listing it as a top risk in its latest SEC filing. Cases of inflated property valuations allowed borrowers to qualify for larger loans, with some loans resold to Fannie Mae and Freddie Mac. JLL also suffered an $18 million hit linked to fraudulent loans sold to Fannie Mae.

Zoom in: While Fannie didn’t disclose the total losses from fraud, its Q3 report highlighted the impact on a $600M portfolio of multifamily loans that is now severely delinquent. The delinquency rate on this portfolio rose from 0.46% at the end of 2023 to 0.56% by September 30, 2024, with around one-third of these loans—particularly in senior housing—being over 60 days past due.

Impact on financials: Despite these challenges, both agencies posted positive Q3 results. Fannie Mae reported $4B in net income, financed 103,000 affordable units, and grew its net worth to $90.5B. Freddie Mac’s net income reached $3.1B, having financed 131,000 rental units—94% affordable for low- to moderate-income households—and seeing new business rise to $15B as demand responded to lower rates.

Concerns remain: However, steady profits haven’t yet alleviated broader financial concerns. Both agencies continue working to build reserves sufficient to withstand economic downturns. Fannie and Freddie’s net worth growth, though positive, still falls short of capital requirements, with regulators indicating a combined need of $319 billion to meet long-term safety standards.

➥ THE TAKEAWAY

Moving forward: Freddie and Fannie’s Q3 results reveal growing demand for multifamily loans, but also highlight ongoing challenges from rising delinquencies and fraud. Expect intensified borrower scrutiny and stricter property valuations as the agencies work to mitigate fraud risks and tighten underwriting practices.

TOGETHER WITH REAP CAPITAL

Reap Capital Secures Major Price Reduction

Reap Capital has secured a $1.55M price reduction on The Calvin, a 167-unit, core-plus multifamily property in Plano, TX—a top DFW submarket. This institutional-quality asset offers value-add returns.

Tax Benefits: 100% depreciation on invested capital for 2024

Low Basis: 32% below seller’s basis and 50% below replacement cost.

Prime Location: $114K median income within 1 mile; walkable to Trader Joe’s, Whole Foods, Pottery Barn, REI, and more.

Upside Potential: Investors receive 80-90% of upside based on Class level.

Closing November 20th. Allocations are granted to investors funding on a first-come, first-served basis. Schedule a call with our team now to learn more.

*Please see the advertising disclosure at the bottom of this newsletter.

✍️ Editor’s Picks

Commercial rebound: Q3 CRE sales volumes either grew or stabilized, led by the office and multifamily sectors, although retail declined, according to Colliers.

Thriving on credit: Brookfield Asset Management raised $21B in Q3, with $14B from credit arm operations, and aims to grow its credit holdings to $600B.

Real estate race: The 2024 presidential election between Kamala Harris and Donald Trump holds major implications for commercial real estate; here is what's at stake.

Market growth: The total US CRE market has reached $26.8T, with alternative sectors like residential and healthcare properties now making up 37% of the investable landscape.

🏘️ MULTIFAMILY

Demand outpaces supply: US multifamily vacancy rates dropped to 5.3% in Q3 as demand outstripped new supply, with strong net absorption of 153.3K units and steady rent growth of 0.3%.

San Jose revamp: The John Stewart Company secured a $30.2M HUD loan to renovate the 192-unit Monte Alban Apartments in San Jose, exceeding the property's estimated value of $25M.

Golden State exodus: California's newcomer inflow hits a historic low of 422,075 in 2023, down 11% from 2022, due to worsening affordability and contentious politics.

Broadway boom: Two mixed-use developments on Broadway and South Broadway in NY, comprising 185 apartments and worth $159M, win some key tax breaks, with 300 jobs expected.

Uptown shuffle: The Hanley, a 150-unit luxury rental building at 165 East 66th Street in NYC, was sold by CIM Group for $128M to Stonehenge.

🏭 Industrial

Data center surge: KKR (KKR) projects global data center spending will reach $250B annually to meet rising AI and cloud computing demands, as firms like Blackstone (BX) and Brookfield (BN) join in.

Industrial headwinds: The US industrial market saw vacancy rates go up to 6.4%, with 4.3% rental rate growth but a low development pipeline.

Chinese retail boom: Chinese demand for US industrial leases surged this year, with China-based logistics firms leasing 20% of available new warehouse space.

🏬 RETAIL

Friday fiasco: TGI Fridays filed for Chapter 11 bankruptcy in Texas, listing assets and liabilities between $100M–$500M due to COVID complications.

SoHo Surge: Retail investment in SoHo skyrocketed with $259.8M in sales this year, driven by rising rents, robust tourism, and high demand from luxury and international buyers.

Luxury slowdown: European luxury giants like LVMH are reporting empty stores in China as Chinese consumer lose their appetite for high-end goods amid a struggling economy.

🏢 OFFICE

Optimistic leasing: Major landlords in Metro Atlanta are seeing increased leasing activity. In Q3, almost 500KSF was leased, and the YTD total is already 7.2 MSF.

Joining the Spiral: Private equity giant TPG leased 301.3 KSF in Tishman Speyer’s Spiral building at Hudson Yards, marking October's largest office relocation in NYC.

Cooling tenant costs: Office tenant costs in North America inched up 0.4% last quarter, with rent declines and stabilizing fit-out expenses hinting at potential cost relief for occupiers next year.

🏨 HOSPITALITY

Earnings miss: Marriott's (MAR) Q3 profit fell short of forecasts, prompting a lower full-year outlook. Modest hotel demand and an adjusted EPS of $2.26 underwhelmed analysts.

From hotels to homes: Oakland Alameda Hotels plans to convert a $15M hotel near Oakland Stadium into homes after its value dropped by 80%.

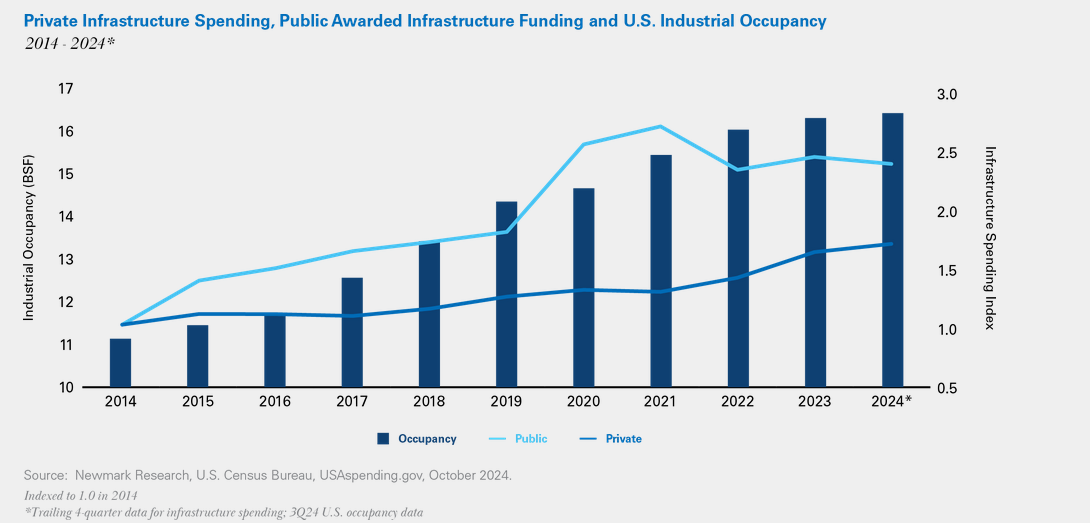

📈 CHART OF THE DAY

U.S. industrial spending and funding have grown steadily from 2014 to 2024, rising from around 11 BSF to nearly 16 BSF, aligned with significant boosts in both public and private infrastructure spending.

Public infrastructure spending soared over the last decade, reflecting substantial federal investment such as the Bipartisan Infrastructure Law enacted in 2021. Private infrastructure spending, although lower, also shows consistent growth over the period.

This ramp-up in spending has supported industrial expansion. Remaining infrastructure funds are expected to pour in until at least 2027, potentially boosting spending even more as interest rates ease.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |

Reply