- CRE Daily

- Posts

- Lenders Race to Buy Back Delinquent Multifamily Mortgage Loans

Lenders Race to Buy Back Delinquent Multifamily Mortgage Loans

As delinquencies mount in multifamily mortgages, lenders are racing to buy back CRE CLOs.

Jordan B.

May 02, 2024

Together with

Good morning. In Q1 of 2024, lenders repurchased $520M in delinquent multifamily mortgage loans to keep the share of bad debt from spiking too high. Meanwhile, the West is rebounding, emerging from 13 straight months of falling rents to achieve an annual increase.

Today’s issue is brought to you by BV Capital.

Market Snapshot

|

| ||||

|

|

bad debt

Lenders Race to Buy Back Delinquent Multifamily Mortgage Loans

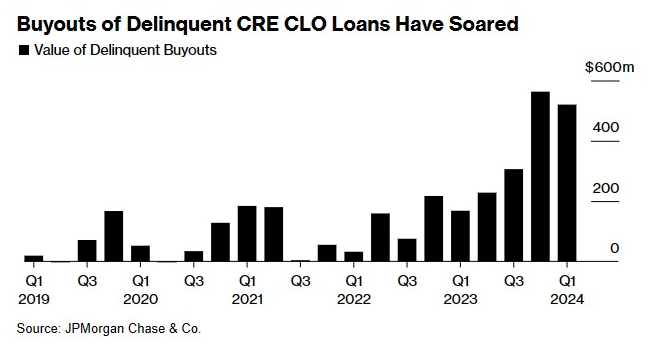

As delinquencies mount in multifamily mortgages, lenders are racing to buy back loans from their commercial real estate collateralized loan obligations (CRE CLOs) to mitigate rising rates.

Stuck on repeat: Lenders have reported a notable rise in loan delinquencies within their CRE CLOs—securities backed by loans primarily secured by multifamily properties. To combat this, in Q1, lenders repurchased up to $520M of delinquent loans, up 210% YoY, an increase from $167.7M during the same period last year. Lenders are utilizing warehouse lines of credit to finance these buybacks, capitalizing on temporarily low financing costs, which could rise if the Federal Reserve adjusts its interest rate policies.

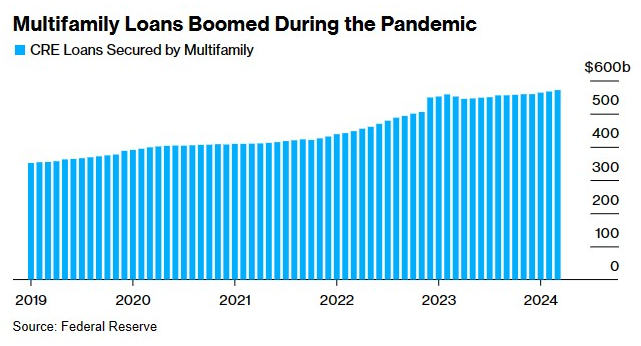

State of the market: The CRE CLO market expanded aggressively, peaking with $45 billion in issuances in 2021, a 137% increase from 2019. This growth was driven by real estate syndicators capitalizing on the pandemic-driven demand in suburban areas. However, the sector now faces headwinds from higher insurance costs and stringent monetary policies, which have led to a 33% increase in distressed multifamily assets, escalating to nearly $10 billion as of March.

The impact: This deterioration has attracted attention from short sellers, particularly impacting firms like Arbor Realty Trust, where short interest has reached record levels.

➥ THE TAKEAWAY

Why it matters: CRE CLOs attract investors because the issuers have more skin in the game compared to CMBS, but they are criticized for comprising more vulnerable, lower-quality loans that are sensitive to interest rate fluctuations. Lenders are buying back delinquent loans to protect their fee revenue and bolster investor confidence in an unstable real estate market. However, the current high interest rates, tightening risk premiums, and the looming threat of federal rate hikes present significant challenges to the financing landscape.

TOGETHER WITH BV CAPITAL

Take Advantage of Rent Growth in High-Demand Texas Markets

Did you know that despite over half a million people moving to Texas since the summer of 2021, multifamily construction starts are down more than 70%?

For investors, this supply and demand imbalance can mean only one thing — opportunity.

BV Capital is a real estate private equity company specializing in ground-up multifamily construction deals in Texas. A vertically integrated company, BV has an in-house construction team that has allowed for historical returns beyond traditional value-add investments.

Sold to accredited investors via a private placement memorandum. Past results do not guarantee future returns.

✍️ Editor’s Picks

FOMC: Fed Chairman Jerome Powell held the line against inflation and kept interest rates steady at 5.25–5.5%, hinting at delayed cuts in 2H24—but only if inflation cools down.

Cracking down: The FTC has officially banned noncompete clauses, impacting up to 32M workers while boosting business formation by 2.7% and worker wages by up to $524 annually.

Debt dial: Distressed CRE levels in the U.S. surpassed $88.6B in 1Q24, up $2.7B from 4Q23, per a recent MSCI report.

Capital conundrum: CRE fundraising has hit a five-year low, with Q1 inflow of capital dropping to $28.5B from $30.8B last quarter.

Urban oasis: Serhant leads sales for 850-unit Williamsburg Wharf, a $600M, 3.75-acre waterfront project looking to upstage the Hamptons.

🏘️ MULTIFAMILY

Housing exposed: Nearly 50% of renter households in the U.S. are cost-burdened, with BIPOC households disproportionately impacted by the widening housing affordability gap.

Two-year plan: The U.S. multifamily sector faces some longer-term challenges, but experts predict rebounding growth and post-2025 opportunities.

Silver tsunami: Welltower (WELL) sees an unprecedented opportunity in senior housing due to a supply-demand imbalance while predicting $1.5B–$6.8B more in staffing costs.

Property pain: NYCB's defaulted loans hit $800M in Q1, increasing the pressure on CRE lenders and regulators.

Follow the money: Syndicators are targeting professionals like doctors and engineers to fund new multifamily real estate projects through feeder funds.

Sign of the times: East Clarke Place Senior Residence received 26K applications for 84 affordable units in the Bronx, highlighting the critical housing shortage for low-income seniors in NYC.

🏭 Industrial

Cooling trend: Due to oversupply, self-storage demand is down in Atlanta and Phoenix, leading to lower street rates.

Data-driven: NTT Data plans a $42M expansion in Garland, TX, adding a 236KSF building to its 47-acre campus by 2026.

Breaking ground: Goodman Group (GMGSF) begins construction on a 505KSF industrial building in Long Beach, targeting aerospace, manufacturing, and e-commerce tenants.

🏬 RETAIL

Shopping success: First National Realty Partners expands into South Carolina with the acquisition of Sumter Square, a 66,765-square-foot shopping center now operating in 25 states.

Checkout closed: Walmart (WMT) is closing all 51 Walmart Health centers due to cost issues, suddenly impacting healthcare access for countless communities across the country.

Freshening up: Heidenberg Properties Group purchased 243KSF of Colonie Center in Albany for $28M, financed by Provident Bank.

Mall mauling: Macerich, owner of 47MSF in mall properties, reported a $126.7M Q1 loss and defaulted on a $300M Santa Monica Place loan.

Budget battles: NY's state budget allocates $40M for task forces to combat organized retail theft, finally elevating more crimes to felony offenses.

🏢 OFFICE

Return of the King: WeWork is all set to exit bankruptcy by as early as the end of May after court approval of key motions.

All roads lead to: The Manhattan office market saw high activity across the board, with YTD leasing reaching 9.08MSF.

Downtown dilemma: Chicago's 444 N Michigan Ave and 30 W Monroe Street office buildings were offered at steep discounts due to financial distress.

Ageless assets: Doug Agarwal's Capital Commercial is the top buyer of aging, class B Texas office properties, spending $650M on 5.5MSF.

🏨 HOSPITALITY

Concentric collusion: In federal court, consumers accused major hotel chains of software-based price fixing, alleging collusion to achieve ‘supracompetitive’ rates.

Deal of the day: Related Cos. sells W Fort Lauderdale to Blackstone for $98M. The 346-key oceanfront hotel went for $282K per room.

RENTAL MARKET

Cooling Rents Offer Relief Amid Economic Uncertainty

March continued the trend of declining apartment rents, now down for the eighth consecutive month. Yet, the declines were modest, and median rents still hover above pre-pandemic levels, showing a resilient rental market.

By the numbers: According to a new report from Realtor.com, nationally, median rents across all unit types decreased by -0.3% year-over-year. The median rent stood at $1,722, only $36 less than the August 2022 peak and $313 more than in March 2019. Specifically, studio rents dropped by 1.4% to $1,435, while one-bedroom units decreased slightly by -0.1% to $1,602, and two-bedroom units fell by -0.5% to $1,908.

Midwest: Rents were stable overall, with standout growth in cities like Chicago (+4.3%), Kansas City, MO (+3.4%), and Indianapolis (+3.3%). However, Chicago's median rent was still approximately $1,000 less than those in New York or Los Angeles.

South: The region recorded -1.5% decrease in median rents due to an increase in housing supply, even amidst high demand and low unemployment.

West: After 13 consecutive months of declines, the West saw a slight recovery with a 0.4% increase in rents year-over-year. San Diego and Los Angeles saw rents rise by +2.9% and +1.6%, respectively, while Phoenix and Denver experienced declines of -3.2% and -1.9%.

Northeast: Strong labor markets drove a +3.8% increase in median rents in New York and a +3.3% increase in Boston, reflecting a tight mismatch between supply and demand.

➥ THE TAKEAWAY

It's not as bad as it looks: Although rental prices are slightly declining, the rental market continues to exhibit strength, particularly in major metropolitan areas. High interest rates are prompting potential homebuyers to delay their purchases and continue renting, potentially propping up rental costs. The report emphasizes the need for more housing construction, particularly in the Northeast and West, to ease the home supply shortage.

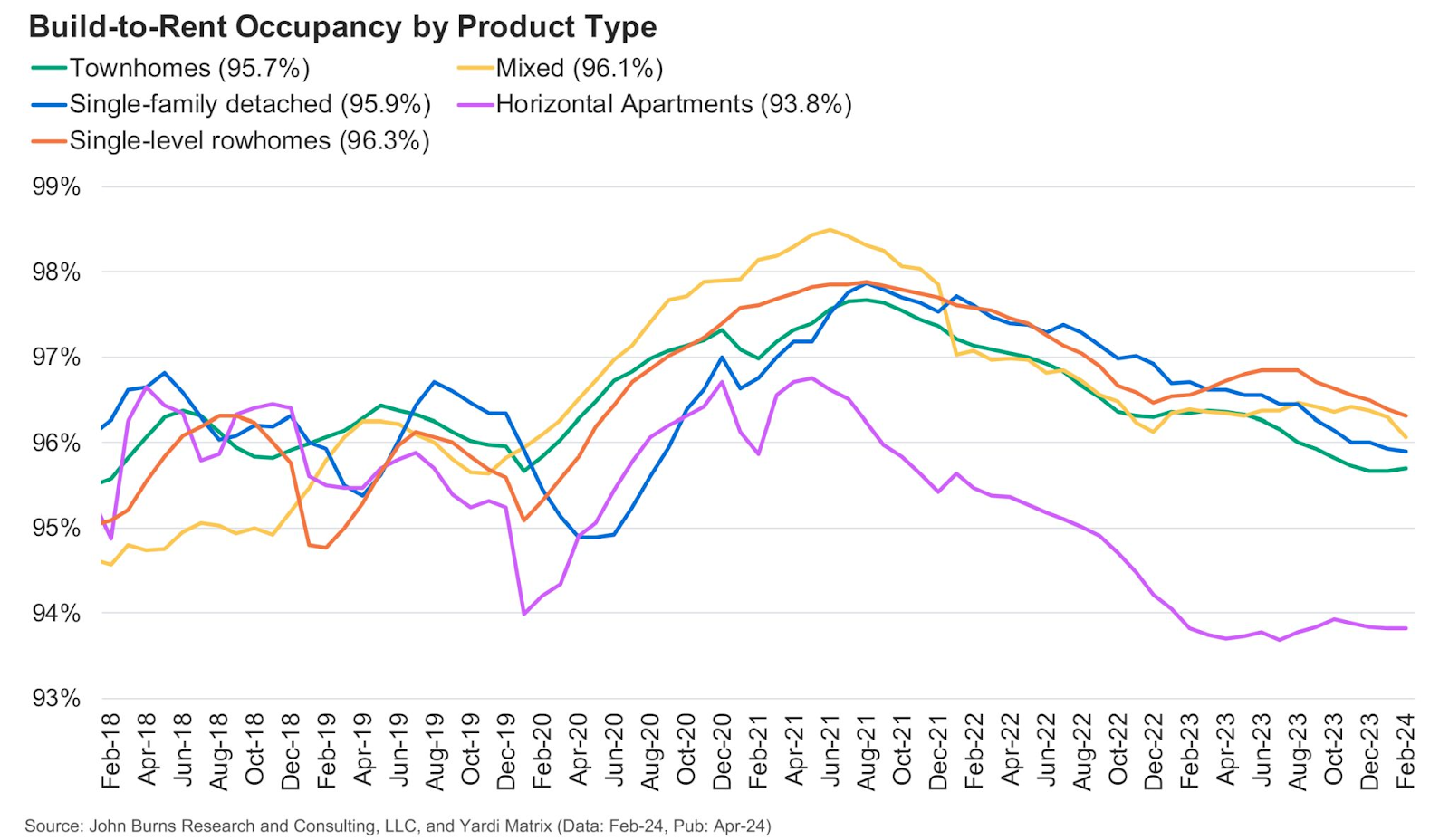

📈 CHART OF THE DAY

According to John Burns, horizontal apartment occupancy is declining much faster than other BTR categories because:

Horizontal apartments are cheaper but also compete more with traditional apartments.

Despite the higher cost, detached homes and townhomes are popular as BTR assets due to high occupancy rates.

BTR typically targets different demographics from traditional apartments, explaining its higher occupancy rates.

Phoenix faces intense competition in horizontal apartments, leading to rent fluctuations.

Will BTR development strategies change? Hard to say—downsizing may not be the best move, as renters prefer larger, pricier options.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |

Reply