- CRE Daily

- Posts

- Yardi Matrix Outlook Reveals Economic Hurdles for Multifamily in 2024

Yardi Matrix Outlook Reveals Economic Hurdles for Multifamily in 2024

A new Yardi® Matrix report predicts a robust multifamily market in 2024, but anticipates challenges in rent growth due to a slowing economy and an increase in housing supply in certain regions.

Jordan B.

December 21, 2023

Together with

Good morning. According to a new report from Yardi, the multifamily sector is expected to remain strong in 2024. However, challenges such as slower economic growth and a significant increase in housing supply in certain areas may impact rent growth. Meanwhile, falling CRE values are putting more small US banks at risk of distress.

Today's issue is brought to you by AirGarage. Refer real estate owners and earn a portion of the revenue from their partnered properties.

👋 First time reading? Sign up. | 🎁 Want free merch? Share this. |

Share CRE Daily with your colleagues to unlock the Back of the Napkin Multifamily Deal Screener and earn additional rewards.

Market Snapshot

|

| ||||

|

|

FACE PALM

Yardi Matrix Outlook Reveals Economic Hurdles for Multifamily in 2024

According to a new report, Yardi® Matrix forecasts a resilient multifamily market in 2024, though rent growth faces challenges from a decelerating economy and a surge in supply in some areas.

Economy still standing: In 2024, the U.S. economy remains resilient, with GDP growth at 2.6% in Q3 2023, and a significant increase to 5.2% recently. Job growth remains strong with 2.7 million jobs added over the past year. Consumer spending increased by 3.2% year-over-year, reflecting a stable financial situation despite increasing consumer debt.

The big question: The multifamily market's future largely hinges on the trajectory of interest rates. With inflation above 3%, there's uncertainty about when rates will decrease. The Federal Reserve, observing a lower core inflation rate of 1.8%, is cautious about reducing rates too soon. This uncertainty has stalled commercial real estate transactions. Interest rates are expected to stabilize in early 2024, with possible modest reductions later in the year, indicating a period of weaker economic growth and sustained higher rates for most of the year.

Slow growth ahead: In 2024, the multifamily housing market is poised to experience modest growth, constrained by several factors, including slower job growth, an increasing supply of units, and diminishing affordability in certain markets. The trend represents a shift from the rent increases seen in 2021 and 2022, where rents nationally rose by 23.5% due to increased household formation, particularly in the Sun Belt and suburban areas. However, growth slowed in 2023, with YoY growth dropping to just 0.4% by November.

Challenges ahead: The 2024 multifamily market faces a slowdown due to a record 510,000 new units increasing supply, causing a minor dip in occupancy rates to 94.9%. Affordability issues are rising, with rent-to-income ratios at 29.8%. While luxury rents decline, rents for more affordable units increase by 2%. This shift, along with costly homeownership, leads to fewer tenants buying homes, maintaining a preference for renting. Consequently, a modest national rent growth of 1.5% is anticipated.

Tread with caution: In the capital markets, the impact of higher interest rates is clearly visible, with property sales slowing down and debt becoming more costly and scarce. This trend marks a significant change from the record-high sales of $228.3 billion in 2021 and $196.9 billion in 2022 to just $57.6 billion in 2023, a 70% year-over-year decline. The primary cause isn't liquidity but the effect of rising interest rates and uncertainty in pricing, leading to a decrease in property values and difficulties in price discovery. Apartment REIT values have also dropped, and with interest rates expected to hover around 4-5% through mid-2024, a sluggish deal flow is anticipated.

➥ THE TAKEAWAY

Looking ahead: 2024 presents a challenging year for the multifamily market, with the necessity to maintain occupancies and control expenses amidst a sluggish economy and tightening capital markets. This shift marks the end of an era where rising market conditions uniformly benefited all properties. Acquisition activities are expected to slow, with the focus shifting toward debt investments and capital for restructuring. For more insights, read the full report here.

A MESSAGE FROM AIRGARAGE

A Win-Win Referral Program

Introducing the new AirGarage Referral Partner Program!

Do you know parking facility owners?

AirGarage is launching a new referral program that will reward you with uncapped commission payouts for introducing us to property owners that sign a new lease or management agreement with AirGarage.

AirGarage’s referral process is easy, just make a warm introduction to property owners in your network and you’ll earn up to 3% of the total parking revenue generated at the property for a period of 24 months.

AirGarage is actively seeking referral partners in all 50 states & Canada. Apply to become a referral partner today!

TRENDING HEADLINES

STR outlook: According to AirDNA, a positive shift for hosts and investors is coming in 2024, following a challenging 2023, buoyed by an averted recession and favorable economic forecasts.

Money markets strain: A sudden increase in U.S. overnight lending rates has caused alarm, suggesting potential liquidity challenges.

Business travel returns: New York's tourism is rebounding strongly in 2023, with a projected 61.8 million visitors, nearing 93% of its 2019 peak, despite ongoing struggles in office occupancy rates.

Uphill battle: Apartment operators face challenges in maintaining occupancies amid a slowing economy, including a wave of deliveries and rising mortgage rates.

Capital of defaults: New CRE loan originations in Q3 were $2.5B, down from $4.7B in Q2, and DC now has more office properties at default risk than San Francisco.

Tax relief rains: The IRS waives $1B in late-payment penalties for 4.6M taxpayers owing back taxes for 2020 and 2021.

Financing feat: JLL's Capital Markets group secured $463M in financing for a $1.2B recapitalization of a 13-property portfolio by Manulife Investment Management and Scannell Properties.

Proptech pains: Investors are growing more cautious about proptech, leading to a 42% drop in venture capital funding in 2023 compared to the previous year.

Oklahoma, arise! Oklahoma City plans to build a 1,750-foot-tall skyscraper, potentially the 2nd tallest in the US, along with other apartment towers and a hotel.

Changing hands: IBM sold a portion of its IBM 500 Campus in Durham, NC, for $66M to Hines Global Income Trust (ZHGIIX), with plans for future mixed-use redevelopment.

Joining the club: The number of accredited investors in the US has grown 16x since 1983, reaching 24.3M households by 2022, according to a report by the SEC.

Unequal opportunities: Over $48B has been invested in 4K Opportunity Zones across the US, but just 1% of those zones received 42% of all investments.

Substantial slide: A Brookfield-owned office building in Downtown LA now worth $210.7M, 53% less than its purchase price, just defaulted on a $275M CMBS loan.

Fancy funding: Luxury fitness chain Equinox is in talks to raise $1B with Goldman Sachs (GS) and Centerview Partners, ahead of $1.5B in debt maturities.

Downtown revival: Developer Stockdale Capital Partners plans to add 850 apartments to its $550M mixed-use redevelopment of a former Westfield mall in downtown San Diego.

DEADLY DEBT

Falling CRE Values Pose Solvency Risks for US Banks

Photographer: David Paul Morris/Bloomberg

Falling CRE values are leading to solvency risks for numerous US banks, as more buildings get pushed into negative equity.

Report readout: According to a report for the National Bureau of Economic Research, 14% of all CRE loans and 44% of office loans are in "negative equity," where debt surpasses property values. This means borrowers are less likely to repay loans, which could mean that "dozens to over 300" smaller US regional banks are at risk of solvency runs.

The risk scale: US banks held approximately $2.7T in CRE debt by the end of 3Q23. CRE values have fallen by 22% since 1Q22, with office prices plummeting 35% due to weakened demand for desk space caused by the widespread adoption of remote work.

Impact of interest: Recent interest rate hikes contributed to the failures of Silicon Valley Bank and Signature Bank and led to the distressed sale of First Republic Bank. Deposit outflows and the banks being left with illiquid, low-yielding loans were significant factors in these events.

Potential losses: If the CRE default rate reaches 10%, it could mean $80B in additional bank losses. According to the report's analysis, if defaults climb to 20%, the losses could increase to an estimated $160B. Comparatively, during the GFC 15 years ago, delinquency rates on CRE loans peaked at around 9%, and charge-offs reached 3.3%.

➥ THE TAKEAWAY

Be careful: The report’s findings have significant implications for financial regulation, risk supervision, and the transmission of monetary policy. The increasing solvency risks small US banks face in the CRE slump highlight the importance of closely monitoring loan portfolios and implementing adequate risk management strategies. Financial regulators need to be vigilant in overseeing these risks.

AROUND THE WEB

📖 READ: College football has always been big business in the US, and short-term rentals are starting to overtake college towns, serving the ever-increasing demand from fans and investors.

🎧 LISTEN: Bert Crouch, Head of NA for Invesco Real Estate, talks CRE prices and the Fed on this episode of The Tape from Bloomberg.

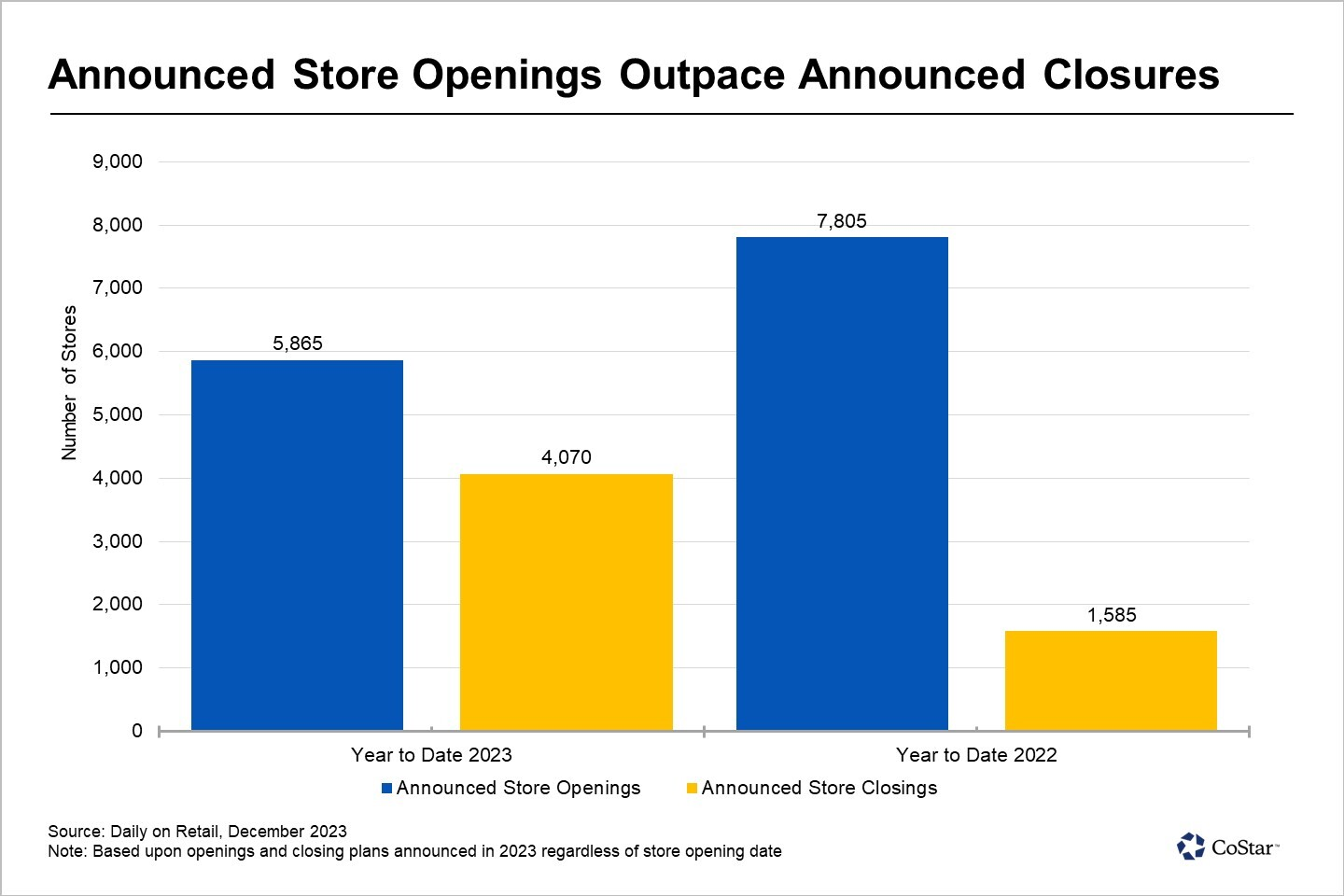

CHART OF THE DAY

Despite the onslaught of retail bankruptcies in 2023—including Rite Aid, Party City, Bed Bath and Beyond, Tuesday Morning, and David's Bridal (RIP)—there have been 44.1% more store openings than store closings overall.

What did you think of today's newsletter? |

Reply